Latin America’s financial sector is undergoing a structural shift driven by both necessity and competition. Across the region, more than 200 million adults remain unbanked, underbanked, or lack sufficient credit history to access formal financial services, while serving geographically dispersed populations has historically made traditional banking models costly and difficult to scale.

At the same time, a younger, mobile-first population is accelerating the adoption of digital financial services. Superapps and challenger banks across markets like Brazil, Mexico, and Colombia are reshaping customer expectations, placing pressure on incumbent institutions to rethink how they acquire, serve, and retain customers.

Within this environment, the ability to expand access to credit is becoming a defining factor in competitive positioning. Financial institutions are no longer competing solely on products, but on their ability to reach and underwrite previously inaccessible segments.

This shift is explored further in the whitepaper From Pilots to Production: How Banks Turn Artificial Intelligence into Revenue, which examines how institutions are expanding access while driving measurable business outcomes.

[Download this whitepaper to get exclusive insight]

The Limits of Traditional Credit Systems

For decades, credit underwriting has depended on structured financial data. Credit bureau histories, documented income, and collateral have served as the foundation for assessing borrower risk.

In Latin America, however, these inputs capture only a portion of the population. Large segments of individuals operate with limited or non-existent credit histories, despite participating actively in the economy. Many earn, spend, and repay consistently, but do so outside systems that traditional models recognize.

As a result, credit exclusion is not always a reflection of borrower risk. It is often a consequence of incomplete visibility. Financial institutions are constrained not by a lack of opportunity, but by the limitations of how risk is measured.

Expanding Visibility Through Alternative Data

As financial ecosystems become more digitized, new forms of data are emerging that provide a more complete view of borrower behavior.

Payment histories from utilities, mobile usage patterns, rental records, and other behavioral signals offer insights into financial reliability that extend beyond traditional credit files. These signals are particularly valuable for underbanked individuals and borrowers with thin or non-existent credit files, where conventional scoring models provide little coverage.

By incorporating these signals into underwriting models, financial institutions can begin to evaluate borrowers who were previously invisible. The scope of assessable customers expands, allowing lenders to move beyond rigid eligibility criteria toward more inclusive and precise decision-making.

This does not lower risk standards. It refines them.

Artificial Intelligence and Scalable Inclusion

The integration of alternative data introduces complexity that cannot be managed through manual processes alone. Artificial Intelligence enables institutions to process large volumes of diverse data and identify meaningful patterns within them.

Risk assessment becomes more adaptive, allowing institutions to evaluate borrowers based on evolving behavior rather than fixed historical records. This is particularly relevant in markets where financial activity is dynamic and not always formally documented.

As these capabilities are embedded into decisioning processes, financial institutions gain the ability to scale access to credit without proportionally increasing operational burden. What was previously constrained by data limitations turns into an opportunity for expansion.

Case Study: Expanding Access Through Alternative Credit Models

In Mexico, Kueski has built its lending model around the use of alternative data to serve individuals with limited or no credit history. By analyzing behavioral and transactional signals, the platform is able to assess creditworthiness for first-time borrowers who would typically be excluded from traditional systems.

A similar approach can be seen in Brazil, where Creditas has developed lending solutions that leverage alternative data and asset-backed models to reach underserved segments. By expanding the inputs used in underwriting, the company has been able to extend credit more effectively while maintaining control over risk.

These examples reflect a broader shift across Latin America. Financial institutions are increasingly moving beyond conventional data sources to identify and serve new borrower segments, transforming access into a scalable business opportunity.

From Capability to Execution

Despite the availability of data and analytical tools, expanding credit access requires more than model development. The challenge lies in integrating these capabilities into operational workflows.

Decisioning systems must be embedded into the processes used by frontline teams. Without this integration, insights remain underutilized and lending practices continue to rely on traditional methods.

As highlighted in the whitepaper, measurable outcomes are achieved when data-driven decisioning becomes part of everyday operations. Institutions that successfully bridge this gap are able to translate analytical capability into real business impact.

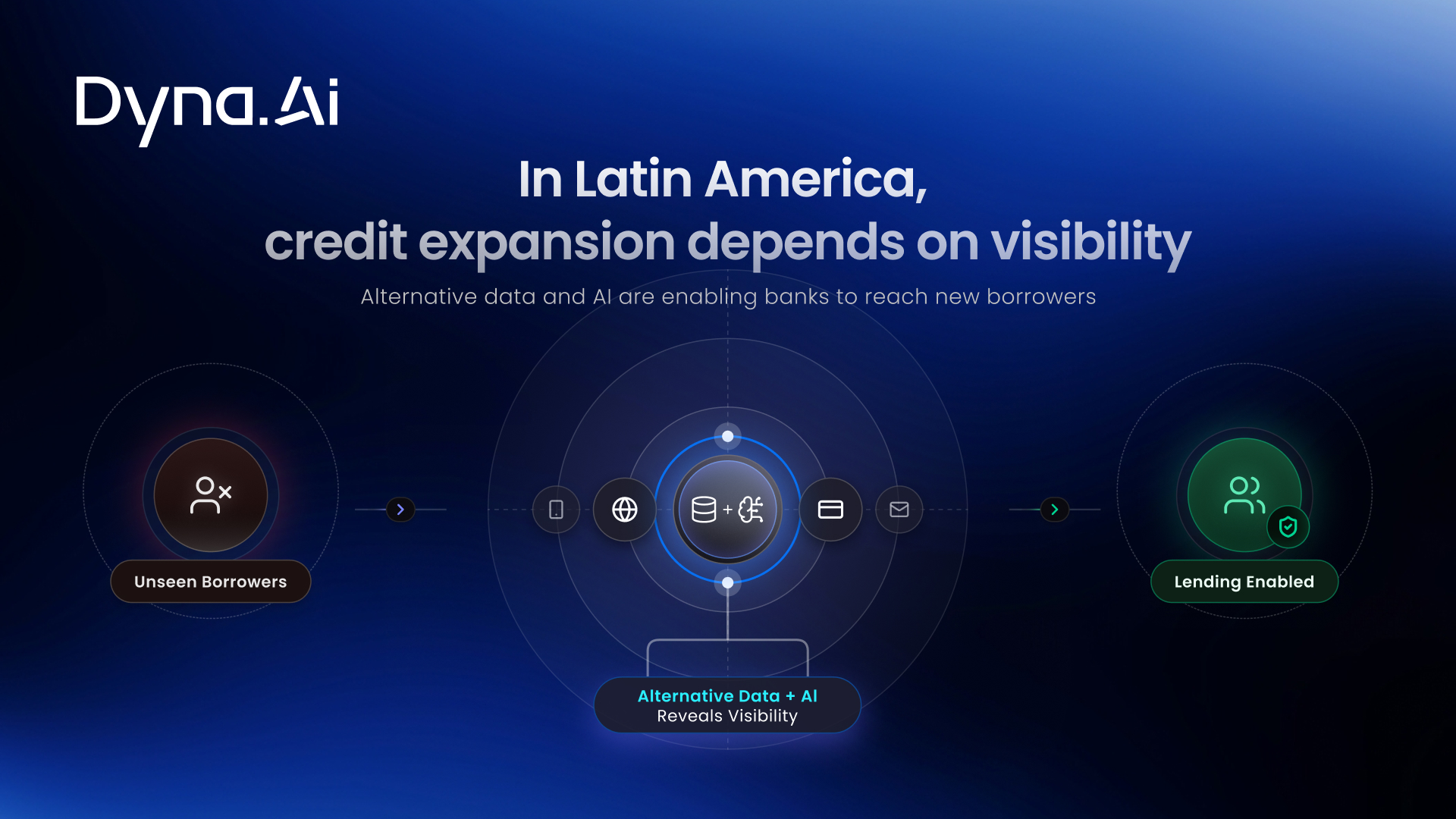

Visualizing the Path to Credit Expansion

This model illustrates how alternative data expands borrower visibility, while Artificial Intelligence enables scalable decisioning. Together, these capabilities allow financial institutions to move beyond traditional constraints and extend credit to unbanked, underbanked, and thin-file populations across Latin America.

From Financial Inclusion to Revenue Growth

As access expands, lending evolves from a constrained activity into a driver of growth. Financial institutions are able to reach new customer segments, increase lending volumes, and diversify their portfolios.

This shift has broader implications. Expanding access is no longer viewed solely as a social objective. It becomes a commercial strategy that supports long-term performance.

In a region where large portions of the population remain outside formal financial systems, the ability to underwrite these segments effectively represents one of the most significant opportunities for growth.

Explore the Full Research

These themes are explored further in the whitepaper From Pilots to Production: How Banks Turn Artificial Intelligence into Revenue, which examines how financial institutions scale access, improve decisioning, and convert data into measurable business outcomes.

[Download this whitepaper to get exclusive insight]